Overview of the 2023 telecoms market

The review is provided in accordance with the data of the Statistics Committee of the Ministry of National Economy of the Republic of Kazakhstan, marketing data on the communications market from open Internet sources, as well as expert assessments.

Main trends in the telecoms market in 2023

(+14% against 2022)

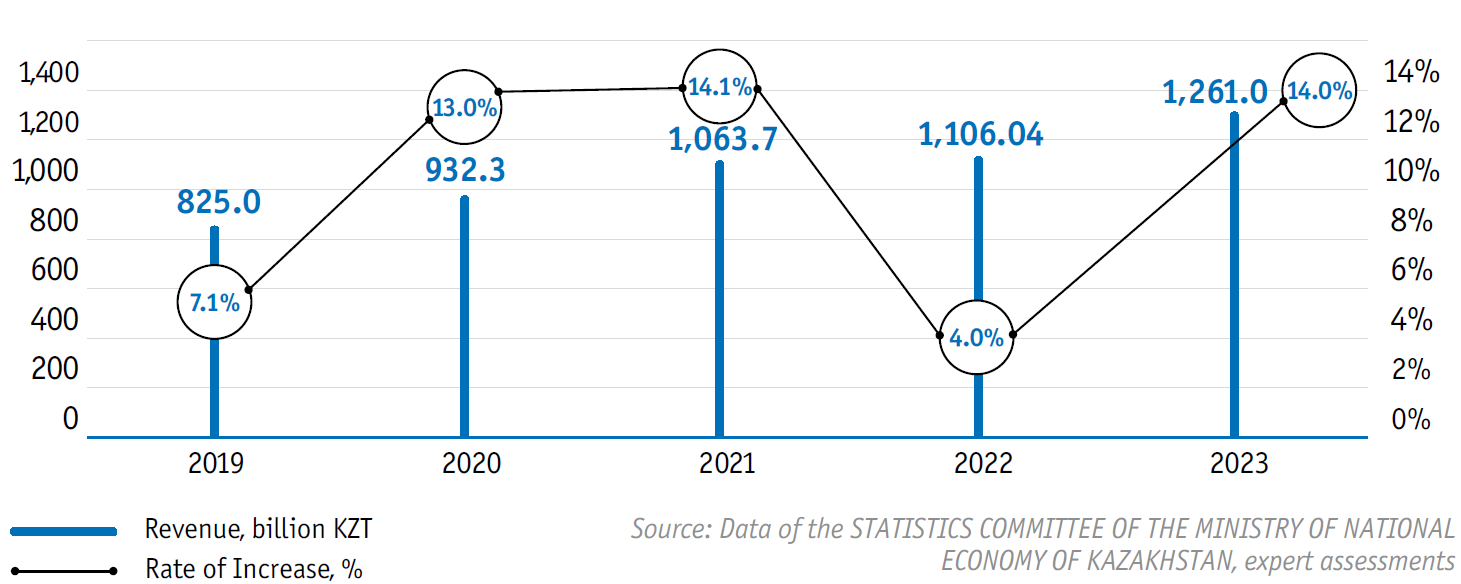

At the end of 2023, the communications services market made KZT 1,261 billion, exceeding the previous year’s figure by 14%.

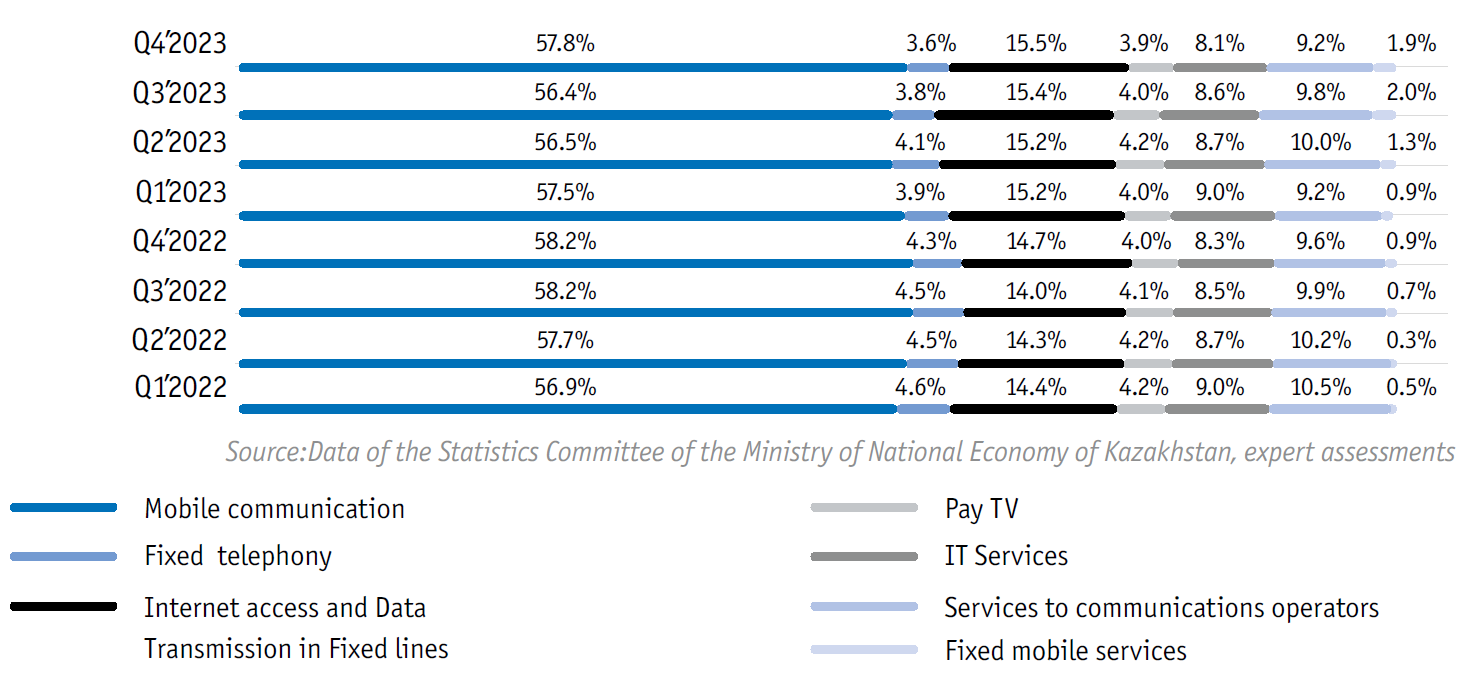

- Mobile communications dominated by type of services. Mobile revenue still generates more than half of the total market volume – 57.8%.

- At the end of Q4 2023, the fixed telephony market volume totalled KZT 44.7 billion, down 6.8% year-on-year in 2022.

- Data transmission and Internet access services in fixed networks showed revenue growth to KZT 195.3 billion. In 2023, the market share was about 15.5%.

- The segment of Pay TV services accounted for 3.9% of total revenues from communication services in 2023.

- Revenues from telecom operators’ services are growing under the influence of structural shifts. As the retail market grows, the volume of telecom operator services increases, which is reflected in the growth of this segment’s share in total telecom revenues.

Assessment of the size and structure of the Kazakhstan telecommunications market in 2023

Kazakhstan’s telecoms market cemented its growth prospects, showing a 14% year-on-year growth in 2023. In absolute terms, the market volume totalled KZT 1,261 billion.

Revenue from communication services in Kazakhstan in 2019-2023, billion KZT

Service revenues in the mobile segment continue to dominate, with their share rising to 57.8% in 2023. The key growth driver for the mobile market is the growth of mobile data transmission and services based on them.

The stable share of revenues from B2O services – 9.2% – is related to the active development of infrastructure by telecom operators in remote areas to reduce the digital divide between citizens.

Positive dynamics in the fixed broadband and data transmission segments, as well as in the IT services segment, keep their contribution to the total market volume at 15.5% and 8.1%, respectively.

Overall, the market structure by service type has not changed significantly compared to 2022.

Revenue structure of the communications industry in Kazakhstan by type of services, %

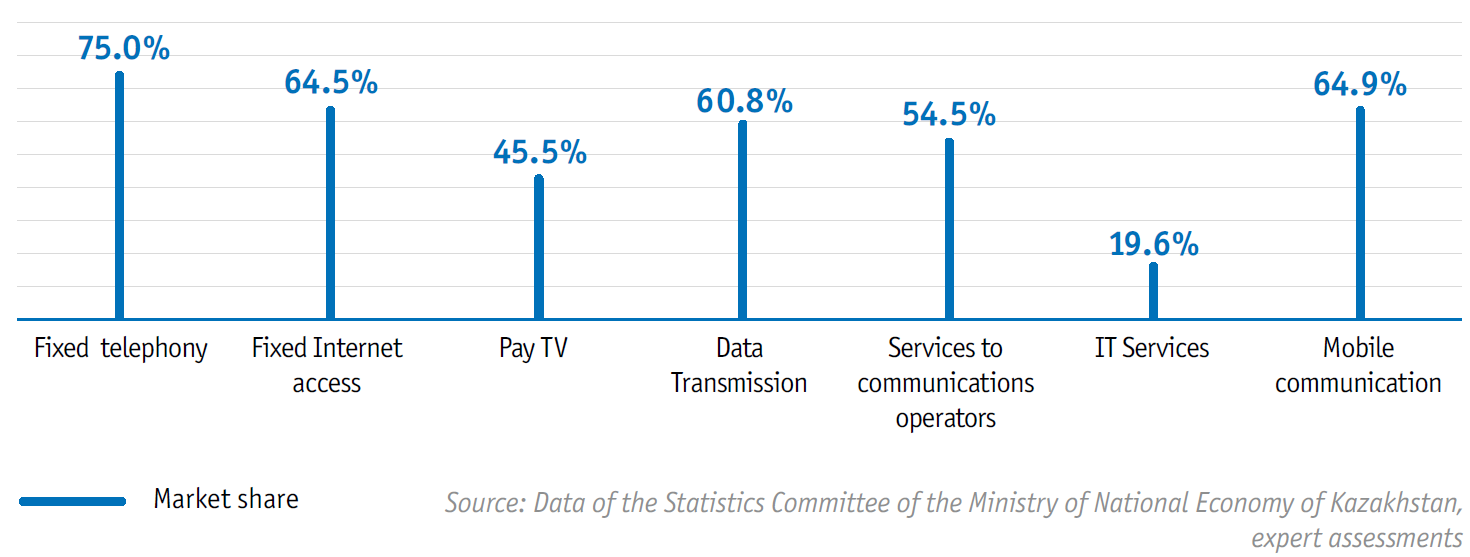

Kazakhtelecom Group’s market position

There was no global change in the balance of forces in the market in 2023, which indicates the established competitive landscape and maturity of the market. The Kazakhtelecom Group market share in 2023 made 61.8%. At the same time, it should be noted that the Beeline Group market share grew from 25.3% in 2022 to 28%. The operator became the leader in terms of revenue both in the mobile segment and significantly increased revenue in the fixed segment. The development of the Company’s IT solutions made a significant contribution to the growth of the operator’s fixed-line revenue.

Positions of the Kazakhtelecom Group by market segment for 2023, %

Fixed telephony

At the end of 2023, the fixed telephony market volume totalled KZT 44.7 billion, decreasing by 6.8% compared to 2022. The reduction in revenues is due to the trend towards mobile and Internet substitution of fixed telephony services, affecting the annual decrease in the consumption of classic wireline telephony services.

In the structure of revenues by type, the largest specific weight with the volume of KZT 28.3 billion falls on local telephony services, being associated with regular balancing of tariff policy by operators aimed at systematic increase in the size of subscriber fees against the background of reduction of tariffs for calls to non-CIS countries. Taking into account the annual reduction of traffic by KZT 2.5 billion on long-distance and international routes, this approach makes it possible to slow down the rate of decline in revenues from fixed telephony services.

Mobile communication

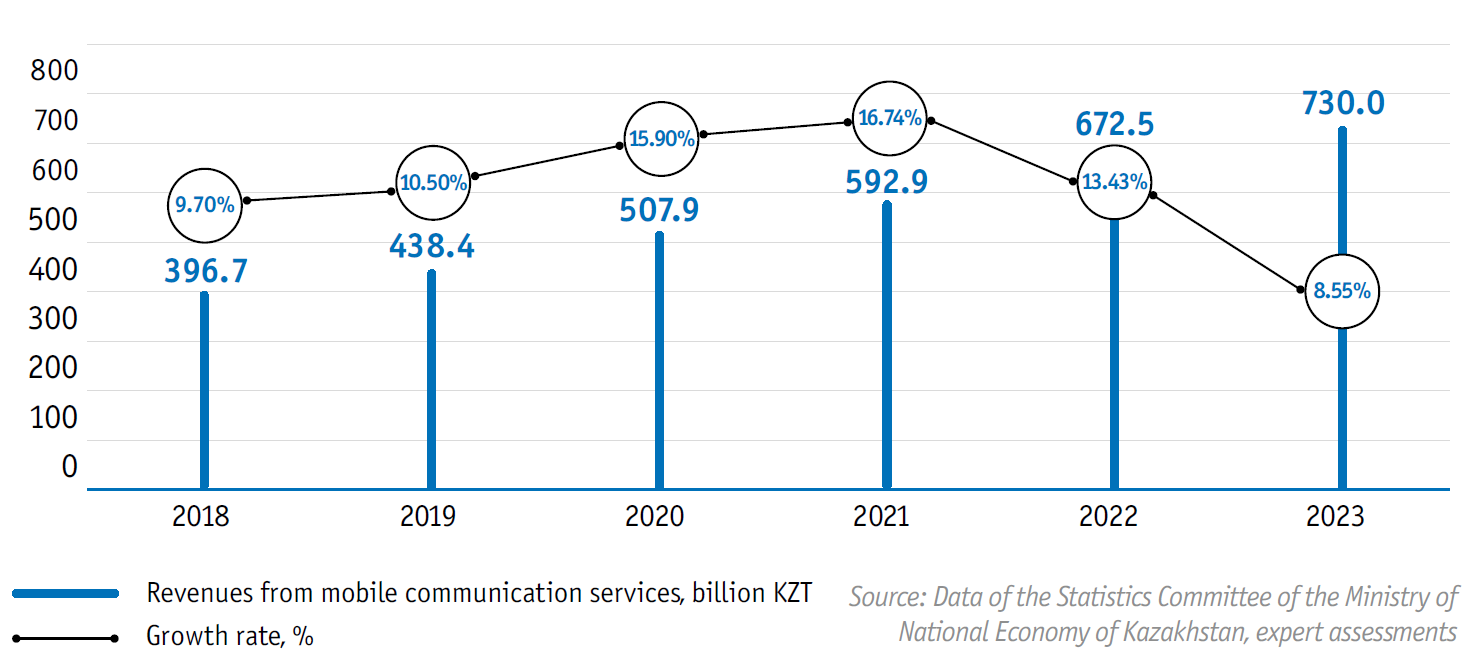

Despite its maturity, the mobile market retains its fundamental role in the development of the telecoms industry, both in Kazakhstan and globally. This is due to the trend towards universal mobility, digitalisation and personalisation of processes – business, social and government interaction. The development of new network technologies and improved quality of mobile data transmission ensure the development of new offers and services, most of which are successfully monetised, which ultimately affects the growth of paid consumption.

At year-end 2023, the cellular telecommunications market in Kazakhstan totalled KZT 730 billion, up 13% year-on-year. The segment’s share of the total telecoms market also strengthened, from 58.2% in 2022 to 57.8% in 2023.

Revenues from mobile communications services in 2018-2023, billion KZT

High-speed Internet access

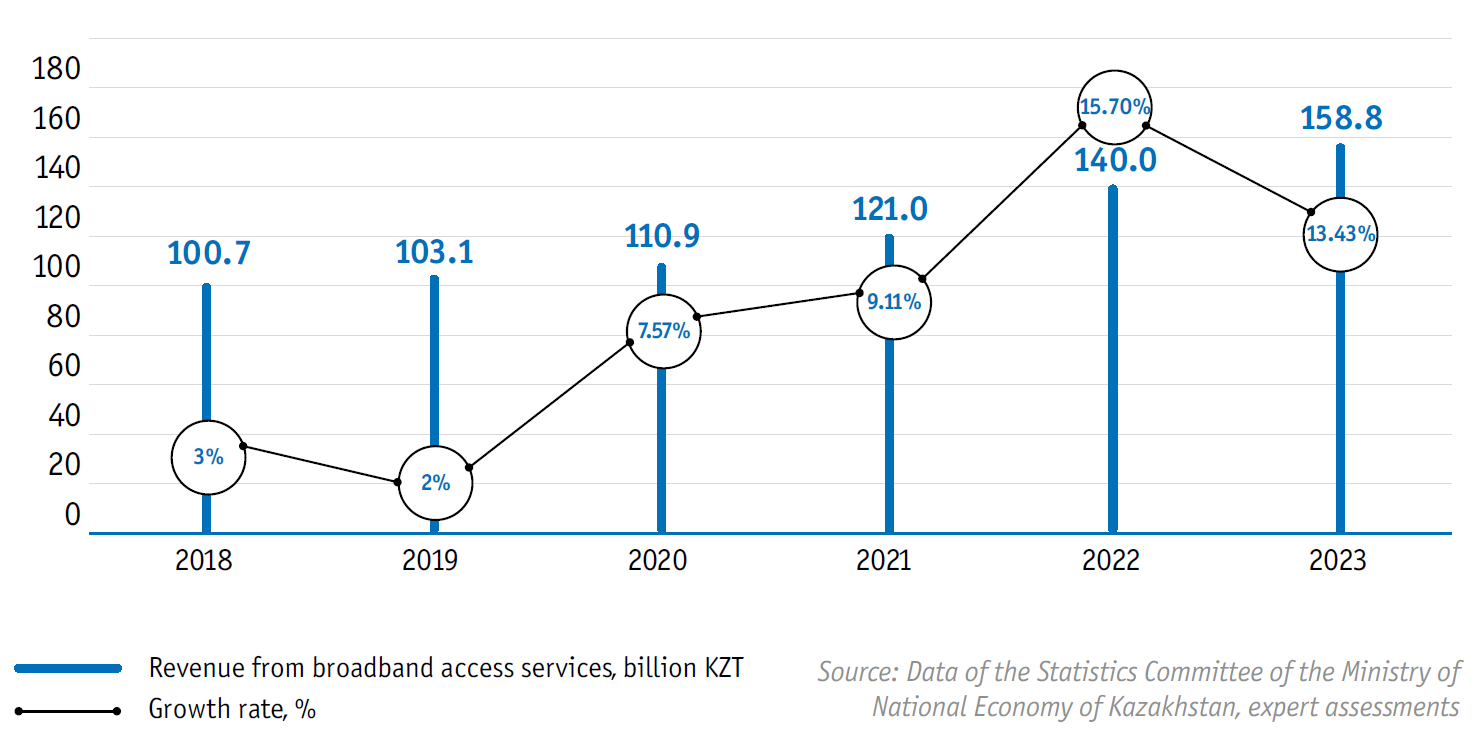

Revenue from broadband access services

The broadband market demonstrates positive revenue dynamics year on year. Despite the fact that the potential of connections in large cities is close to exhaustion, the number of connections continues to grow at the expense of rural settlements. In large cities, ISP operators strive to increase subscribers’ profitability due to migration of subscribers from ADLS connections to FTTx and GPON networks, allowing to increase access speed and volume of provided services and, accordingly, to offer subscribers packages with higher cost for the complex of services at the corresponding cost. Operators providing universal services in rural areas receive appropriate subsidies from the government to compensate lost revenues through the special tariff application. The estimated volume of the fixed broadband market at the end of 2023 is KZT 158.8 billion, which corresponds to an increase of 13.43% yearon- year.

Revenue from broadband access services in fixed networks in 2018-2023, billion KZT

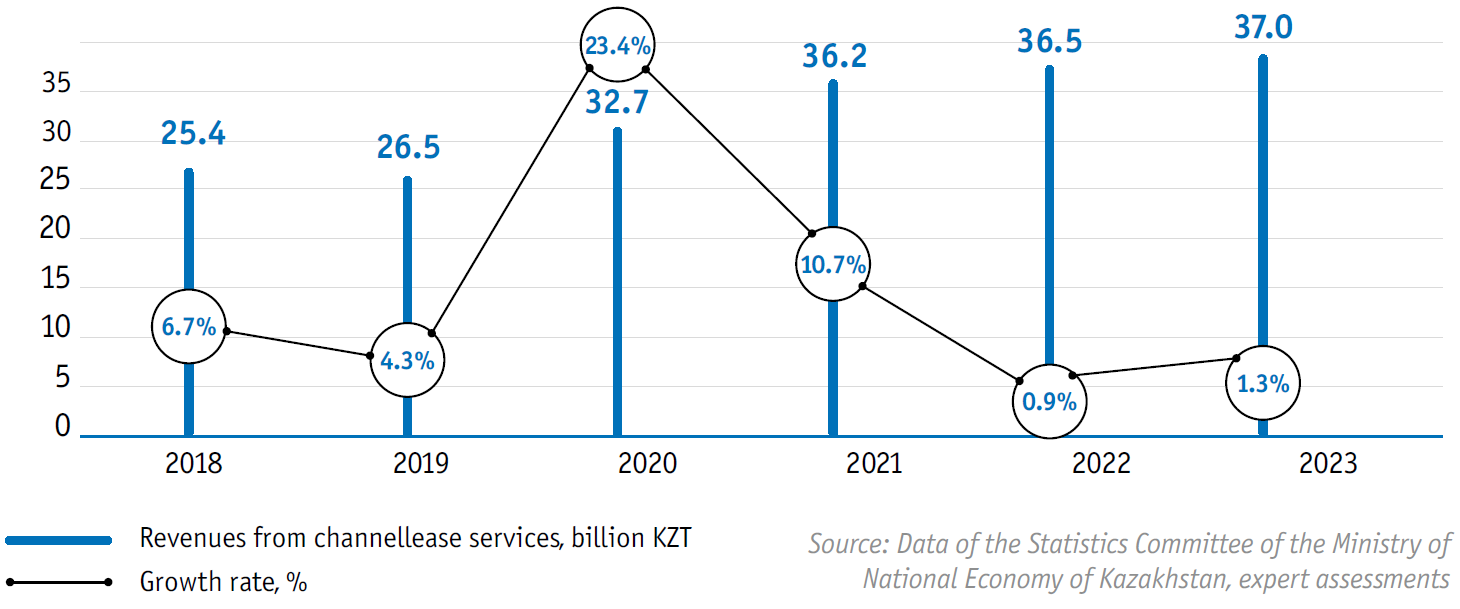

Lease of data transmission channels

The channel lease market, almost entirely based on IP-VPN technology, has been showing signs of stagnation in recent years, despite the fact that the number of branch structures is growing. The DSM task force sees the cloud technologies development and migration of enterprise information systems from local infrastructure to the cloud environment to be the main reason for the reduction in demand for IP-VPN services. This particularly trends in the segment of state-owned enterprises, where complete digital transformation processes are underway.

In the corporate segment, digitalisation is less intensive than in the public sector. This means that the demand for the organisation of communication channels between branches remains, although the volume of new demand is also significantly decreasing.

At the end of 2023, the channel rental market, according to the task force’s estimates, totalled KZT 37 billion, i.e. almost at the level of the previous year.

Revenue from channel lease services in 2018-2023, billion KZT

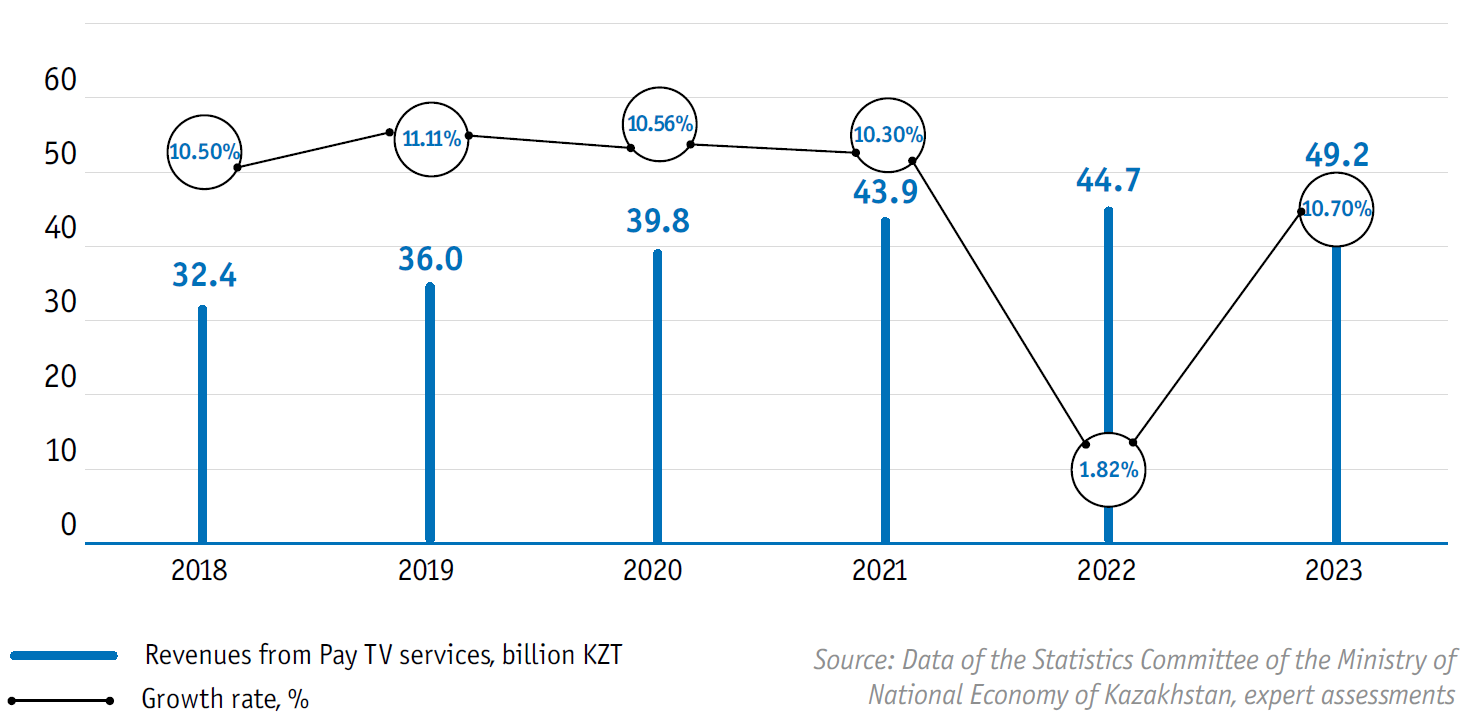

Pay TV

At the end of 2023, operators’ revenue from Pay TV services in Kazakhstan totalled KZT 49.2 billion, up 10% year-on-year.

This volume includes the amount of monthly payments by subscribers for services and equipment rental (STB) and does not include revenue from the purchase of satellite TV sets.

Revenue from Pay TV services is almost entirely generated by households. They accounted for 3% of total revenue in 2023, or over KZT 45 billion. Accordingly, the corporate segment provided services worth KZT 3.5 billion (7% of total revenue).

Revenue from Pay TV services in 2018–2023, billion KZT

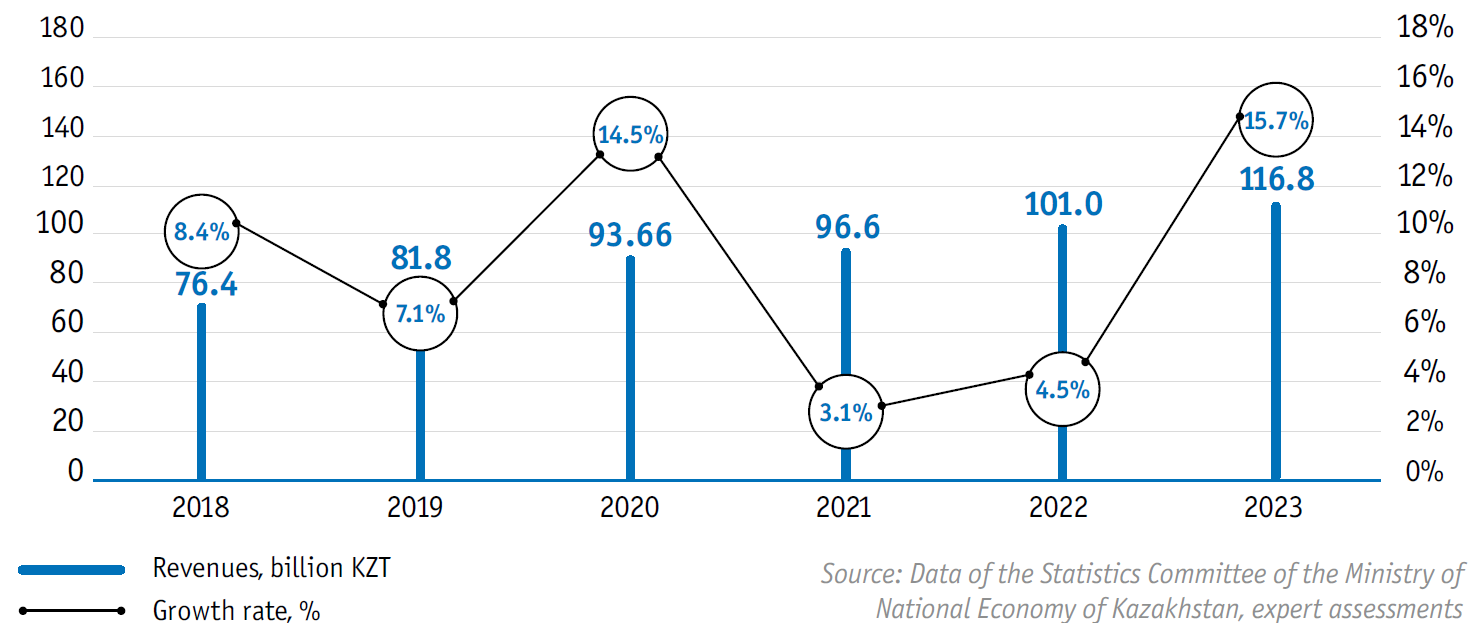

Services to communications operators

In 2023, the market volume and structure of revenue in the inter-operator market did not undergo significant changes compared to the previous year. Aggregate services to operators were rendered in the amount of KZT 116.8 billion, up by 15.7% year on year.

The following major segments generate revenues from services to telecom operators:

- Connection to the public telecommunications network and voice traffic.

- Lease of national and international channels.

- Services on organisation of virtual channels (IP-VPN).

- Internet access for telecom operators.

- Transit of voice and data traffic (IP-transit).

Revenue from services to communications operators in 2018–2023, billion KZT

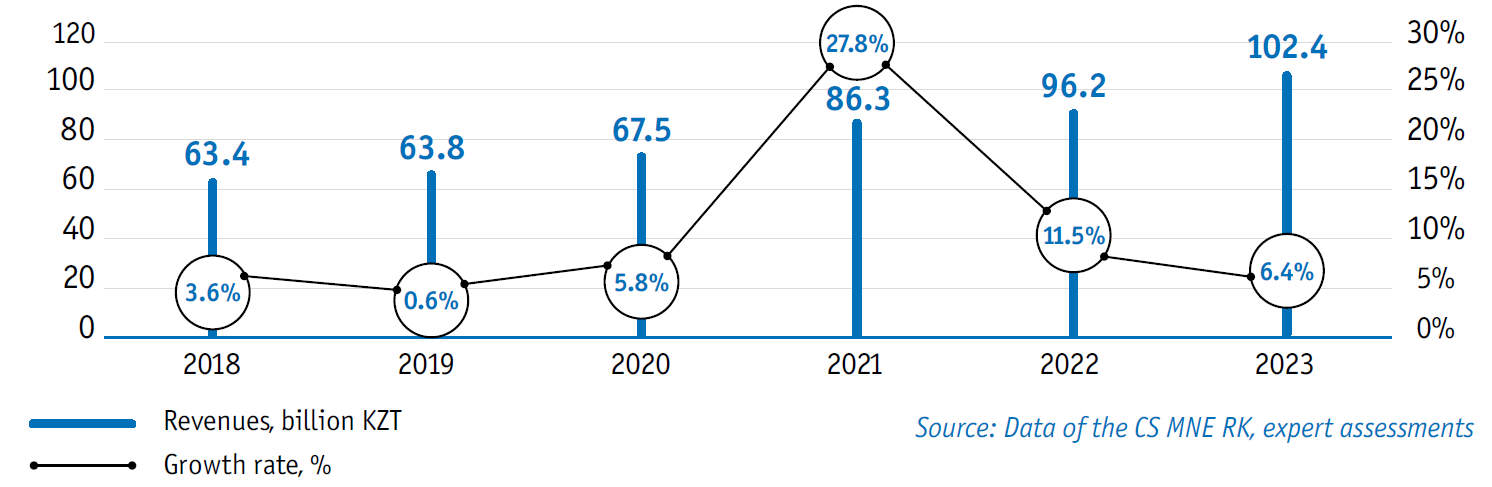

IT services

Against the background of intensive digitalisation of socio-economic processes, as well as interaction between the state and society, the volume of IT services is steadily growing.

In addition to the digital transformation processes taking place within the country, the volume of services provided by Kazakh enterprises is growing due to the export abroad of the Kazakhstan’s developments and IT services. In 2023, services provided by telecom operators account for KZT 102.4 billion.

Changes in revenue from IT services in 2018–2023, billion KZT

The bulk of IT services provided by operators to commercial customers in the open market (outside of government orders or parent company services) is related to the provision of data centre-based services. As additional areas, operators develop cloud video surveillance services, implement IoT-based solutions, and function as fiscal data operators (FDA).